This week, we introduce a new category called “Tax Files.” In these posts, we will share documents we are working on or have found particularly useful in our ERC Caliphal Finances research. These documents address various aspects of taxation, showcasing the diversity of documentation related to fiscal administration and tax concerns.

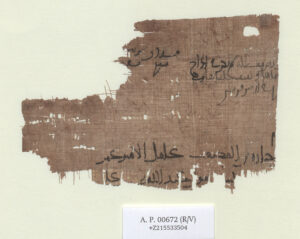

Today, I (PostDoc Noëmie Lucas) am writing about CPR XXI 2, an undated papyrus fragment preserved in the Vienna collection. It was first edited by A. Grohmann (in Aperçu de Papyrologie Arabe, 1932, p. 50 and From the World of Arabic Papyri, 1952, p. 116) and later by G. Frantz-Murphy in CPR XXI (pp. 169-170). It comprises two parts: the top right and left is CPR XXI 2a and the bottom is CPR XXI 2b.

CPR XXI 2

Grohmann and Franz-Murphy interpret this document as a ‘contract of lease.’ The top reads:

Top Right:

Uncultivated land, which will not be included in the kharāj,

its water dried out and its esparto grass pulled out,

faddans 10 in reed land.

Top Left:

faddans for dinars

40 30

This document pertains to fiscal administration, indicating that some parts of the land were not taxed due to being uncultivated and describing the nature of the land. Measurements in faddans and amounts in dinars are mentioned.

Most commentary focuses on the bottom part, where we find the name Junāda b. al-Muṣʿab, the ʿāmil al-amīr of ʿUmar. The rest is hardly readable, but some reconstructions have been made. The most significant is the identification of ʿUmar at the end of the first line of the bottom part. Grohmann, based on his interpretation of amīr, suggests ʿUmar is ʿUmar b. Mihrān, an official in the Abbasid administration during the Barmakid era, reportedly sent to Egypt in 176/792 by Hārūn al-Rashīd to investigate Governor Mūsā b. ʿĪsā. Grohmann asserted that ʿUmar was a governor in Egypt. This has been refined, notably by Michael Dunn in The Struggle for Abbasid Egypt, indicating that amīr in papyrus documents often refers to a financial director. Titles in Arabic papyri are limited, with amīr being common for someone in power. For the Abbasid period, it’s challenging to determine an individual’s position based solely on this title. More importantly, it remains uncertain whether the amīr was a governor or finance director.

However, this document is interpreted as a lease of land. In this context, amīr refers to the individual managing estates in the region, a role falling under the prerogatives of the financial director in Abbasid Egypt, whether or not he was the governor.

I cannot definitively reject Grohmann’s reconstruction since my research on ʿUmar b. Mihrān shows he played a financial advisory role in Egypt briefly (A research article devoted to this episode of the caliphate of Hārūn al-Rashīd will be published, stay tuned!). Yet, I believe it is more likely that the ʿUmar mentioned is ʿUmar b. Ghaylān. He was the financial director at the start of Hārūn al-Rashīd’s caliphate, likely between February 789 and May 791. Sources about him are more varied than for ʿUmar b. Mihrān. Accounts in narrative sources indicate he was involved in distributing stipends to soldiers and likely oversaw the minting of gold coins and regulation of weights and measures.

‘Abbasid Caliphate. period Al-Rashid. AH 170-193 / AD 786-809. AV Dinar (17.1mm, 4.02 g, 6h). Without mint-name (struck in Egypt). bearing the name of ʿUmar

If confirmed, CPR XXI 2 can be added to evidence about ʿUmar b. Ghaylān’s administration, pertaining to his role in estate management. Despite its fragmentary nature, the document seems to relate the top and bottom parts, where the top provides details about the leased land. Besides illustrating the financial director’s role in Egypt, it also shows how the land’s nature influenced tax calculations.

Arabic documents are cited according to “The Checklist of Arabic Documents”.

Banner Image: Free stacks of paper files image, public domain CC0 photo.

Leave a Reply